Figure 1: Modified --drawups can identify instances in the time series where significant jumps have occurred. The co-movement of significant jumps implies distress dependency between the time series, which are used to learn the network structure. In the plot, the first green minimum is recorded as a modified --drawup, while the second is not.

Figure 1: Modified --drawups can identify instances in the time series where significant jumps have occurred. The co-movement of significant jumps implies distress dependency between the time series, which are used to learn the network structure. In the plot, the first green minimum is recorded as a modified --drawup, while the second is not.

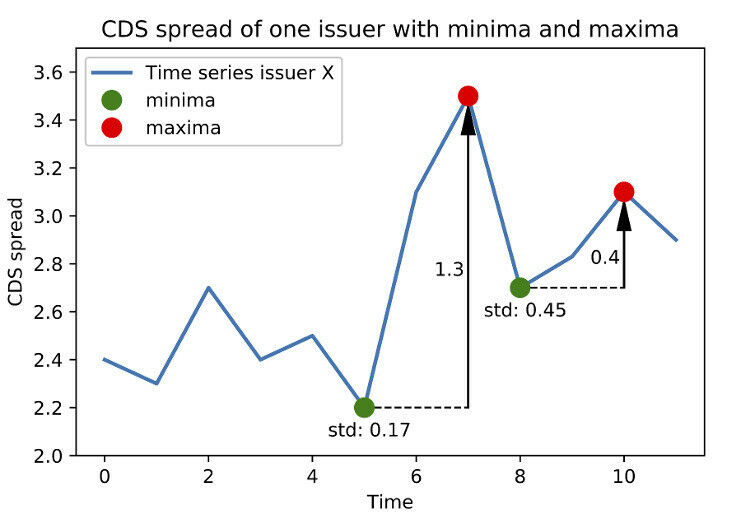

Figure 1: Modified -drawups can identify instances in the time series where significant jumps have occurred. The co-movement of significant jumps implies distress dependency between the time series, which are used to learn the network structure. In the plot, the first green minimum is recorded as a modified -drawup, while the second is not. UvA - Distress initially affecting a small part of the economy can potentially spread to the entire system, as seen in the global financial crisis and most likely reconfirmed during the ongoing corona virus crisis. April 2020 Researchers from the Informatics Institute of the University of Amsterdam have developed data-driven methods that can be used to estimate contagion effects, and incorporated these in computational models for pricing and risk management. Recently two articles have been published in the leading journals in the field of risk management Journal of Credit Risk and the cutting edge series of Risk.net. Sumit Sourabh, Drona Kandhai, and Ioannis Anagnostou of the Computational Science Lab, in collaboration with Markus Hofer and Javier Sanchez Rivero, developed a novel method for estimating financial contagion effects from market data using techniques from computational modelling and machine learning.

TO READ THIS ARTICLE, CREATE YOUR ACCOUNT

And extend your reading, free of charge and with no commitment.

Your Benefits

- Access to all content

- Receive newsmails for news and jobs

- Post ads